Running a business often feels like spinning plates. You need to pay suppliers to produce your product or service, but require sales to generate cash to make payments. It’s a Catch-22 that can make all the difference to your cash flow.

In this article, we’ll explain what is meant by Working Capital Cycle and how, by weighing your current assets and liabilities, you can have greater control over your affairs, allowing you to navigate every business landscape.

What is the Working Capital Cycle?

Working Capital Cycle (WCC) is the time it takes to convert net current assets and current liabilities (e.g. purchased stock) into cash. A long cycle means tying up capital for a longer time without earning a return. Short cycles allow your business to free up cash faster and to be more agile.

Importance of the Working Capital Cycle

If every transaction your business is involved in occurred on the same day, it would be very simple to understand your financial position. However, in reality, there’s almost always a delay between paying for assets, selling inventory or delivering a service, and receiving payment for your goods or work. This can affect cash flow, so it's important to manage the Working Capital Cycle to improve the short-term liquidity and efficiency of your business.

How to calculate your Working Capital Cycle

In order to calculate your Working Capital Cycle, you need to fully understand your current assets. These form the four phases of the Working Capital Cycle.

What are the four general phases of the Working Capital Cycle?

- Cash – Ensuring there is a healthy cash balance by managing cash inflows and outflows of your business

- Receivables – The payment terms for money owed for goods and services

- Inventory – How long it takes to sell your inventory

- Billing - How long you have to pay your suppliers

Working Capital Cycle formula

To calculate Working Capital Cycle, add the number of inventory days to your receivable days, then subtract the number of payable days.

The Working Capital Cycle formula is:

Inventory Days + Receivable Days - Payable Days = Working Capital Cycle in Days

The Working Capital Cycle formula may vary depending on different types of business. For example, a manufacturing business will have more phases than a retailer.

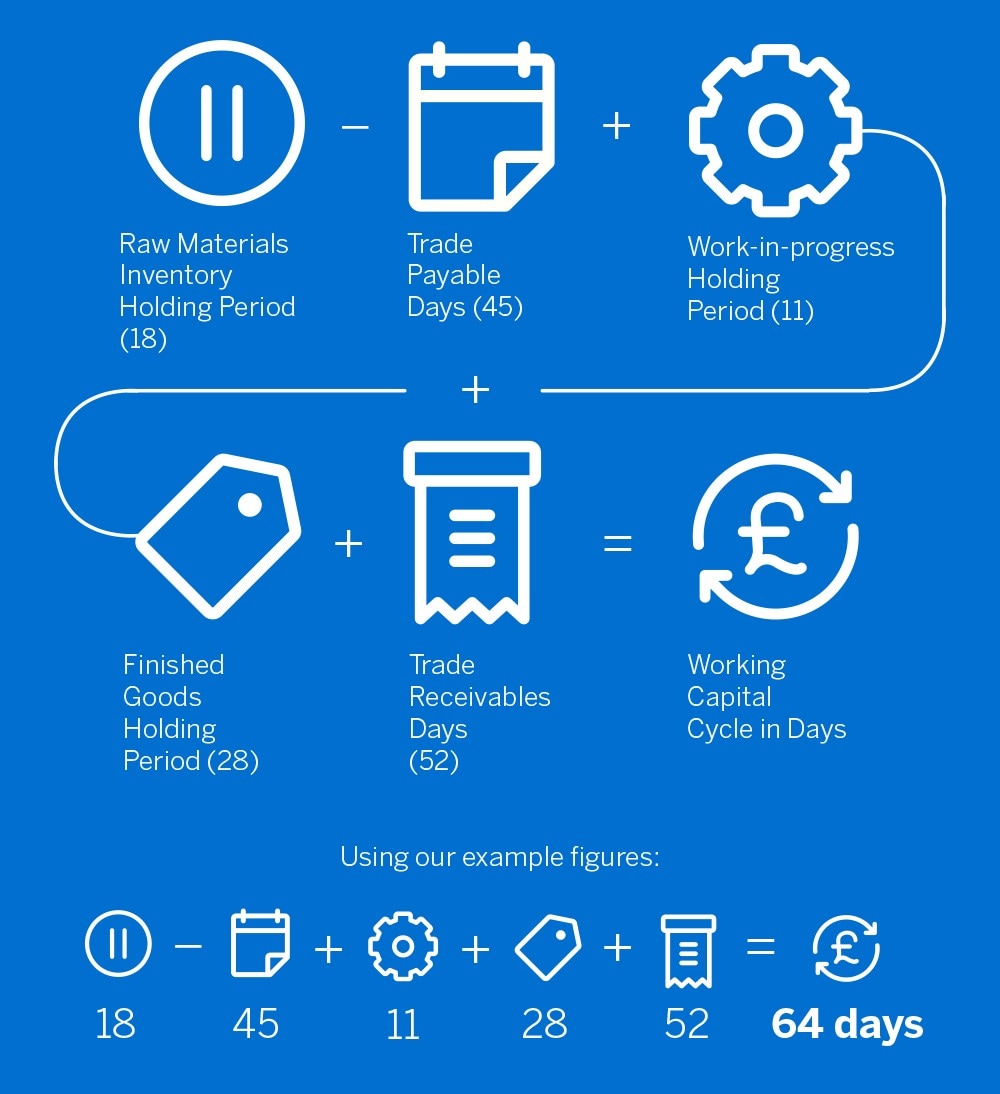

Examples of Working Capital Cycle

Let’s calculate the Working Capital Cycle for a fictitious manufacturing company.

The formula to calculate the Working Capital Cycle for this company is:

This means Maker Ltd will be out of pocket for an average of 64 days between paying its supplier, producing and shipping the product, and receiving cash into its bank account from customers.

However, if Maker Ltd was able to extend the payable days, it would have a shorter Working Capital Cycle and therefore better cash flow. One way to do this would be to negotiate credit terms with its supplier.

Now let’s see what the Working Capital Cycle is like for a retailer. The formula is simpler because a retailer doesn’t need to hold raw materials in stock and turn them into a product.

Supplies Ltd buys furniture from Maker Ltd which they expect to sell in six weeks’ time (Inventory Days). They have 60 days to pay their supplier Maker Ltd (Payable Days), and when a sale is made, payment arrives into their account in three days (Receivable Days).

In our example:

Inventory Days (42) + Receivable Days (3) - Payable Days (60) = A Working Capital Cycle of minus 15 days

What is a positive Working Capital Cycle?

When a company is waiting to receive payment to create available cash, it has a positive Working Capital Cycle. This is normal and the situation most businesses are in because they must balance paying suppliers with producing their product or service, and being paid.

What is a negative Working Capital Cycle?

As we saw in the retailer example above, it is possible to have a negative cycle if you’re able to collect money faster than the time you require to pay your bills.

Why a shorter Working Capital Cycle can be good for your business

A shorter Working Capital Cycle is useful because it lets you free up cash for use elsewhere that would otherwise be stuck in the cycle. In contrast, if your cycle is too long, the capital remains locked in the operational cycle without giving any returns. It’s important to remember that while cash is locked in the cycle, the business needs to have enough capital to sustain its operations, otherwise it could fall into debt and face cashflow problems.

How to relieve pressure on your business by shortening your Working Capital Cycle

A short Working Capital Cycle is achievable in a number of ways. In most cases, it involves several factors in combination.

- Handle inventory in a smart way. Buy stock that’s in demand at a good price and don’t hold too much at once.

- Collect on money owed. Incentivise customers to pay earlier and proactively chase late payments.

- Pay bills on time, but not too early. It’s important to pay suppliers within their payment terms to maintain rapport and keep a healthy credit rating, but there’s little benefit to a working capital cycle if invoices are paid earlier than they’re due.

Despite your best efforts, your working capital cycle will rarely be entirely within your control. For instance, although you can try to negotiate a favourable relationship, you can’t dictate your suppliers’ payment terms.

To help maximise your cashflow, meet your obligations, and take only smart risks to pursue growth opportunities, you could consider an American Express® Business Gold Card, which gives you up to 54 day payment terms¹.

To use a Business Card to extend your Working Capital Cycle, you should line up your supplier payments with your preferred statement cycle. That way, you could have business receivables coming in before business expenses are going out.

1. The maximum payment period is 54 days and is obtrained only if you spend on the first day of the new statment period and repay the balance in full on the due date. If you'd prefer a Card with no annual fee, rewards or other feautres, an alternative option is available - The Business Basic Card.